2019 Trustees Report shows strong bottom line, low cost

The just-released 2019 Social Security Trustees Report lands with a thud – literally – because it’s 270 pages long. But fear not, the key takeaways are straightforward:

- Social Security has a large accumulated surplus – totaling $2.9 trillion – that is sufficient for 100 percent funding until 2035. Looking out a bit further, the Trust Fund stands at 93 percent funded over the next 25 years, 87 percent for 50 years, and 84 percent funded for 75 years.

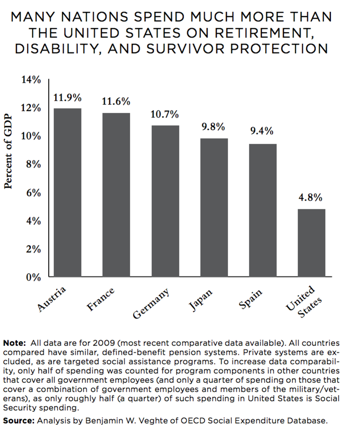

- Social Security is extremely affordable – and will remain that way. By 2095, Social Security will constitute just 6.07 percent of GDP. That is considerably less than Germany, Austria, France, and most other industrialized countries spend on their counterpart programs today.

There is still much room for improvement, both to Social Security’s finances and its benefits. While it’s common for pundits to state that Congress has no plan to address Social Security’s projected shortfall, that is no longer correct.

It is true that Congressional Republicans have no plans – at least, none they seem willing to publicly embrace. Perhaps that is because their preferred “solutions” involve cutting benefits, which is overwhelmingly opposed by voters across the political spectrum.

By contrast, congressional Democrats have introduced several measures. Two of them – the Social Security 2100 Act, introduced by Rep. John Larson (CT), and Social Security Expansion Act, introduced by Sen. Bernie Sanders (VT) – merit special mention. Both bills would not only ensure all promised benefits are paid in full and on time for the foreseeable future – they would also implement more sensible cost-of-living adjustments for seniors, increase Social Security’s modest benefits, and lift the cap on taxable earnings to ensure the wealthy pay their share.

Rep. Larsen has already held hearings on his bill, and Social Security’s future more broadly — and if you’re looking for further confirmation that Democrats are serious about improving Social Security, there’s also this: nearly every 2020 presidential candidate serving in Congress is a member of the bicameral Expand Social Security Caucus.

As well they should! With over half (52 percent) of American households headed by someone of working age who will not be able to maintain their standards of living in old age (rising to roughly two-thirds when health and long-term care costs are also considered), expanding and improving Social Security is the obvious solution to a looming retirement income crisis.

Workers, if they’re lucky, have 401(k) and other retirement savings plans, which studies have proven inadequate, while traditional employer-sponsored defined benefit pension plans are disappearing. Around half of households aged 55 or older (46 percent) had zero retirement savings in 2016. Indeed, 41 percent of American households headed by someone aged 35 to 64 is projected to run out of money in retirement.

It wouldn’t take much of an increase to the average Social Security check to make a big difference to Americans. Social Security’s benefits are modest: the average amount received by Social Security’s over 63 million beneficiaries was only about $16,000 over the past year.

We can do better. Social Security’s benefits are (nearly) universal, the program is incredibly efficient, and the benefits are guaranteed. The case for expanding and improving the program is overwhelming. The question of whether to do so isn’t about affordability – it’s about our values as a nation, and those of whom we elect to represent us in office.

{kind=link}